Context

Climate Ventures, which has been mapping the green economy in Brazil for eight years, has evolved by focusing on bioeconomy and climate technology, specializing in topics such as socio-bioeconomy, nature-based solutions, and regenerative agriculture.

This initial visualization synthesizes methodology, diagnosis of the two universes, capital flows, integration bridges, and the geographical paradox of the Amazon–Cerrado–Atlantic Forest, concluding with a strategic portfolio for each biome.

Map of the ecosystem of Nature-based Solutions

An in-depth analysis of its network of 1,742 organizations and over 27,000 connections reveals a vibrant and mature ecosystem of Nature-Based Solutions (NBS). This ecosystem is, fundamentally, an accurate microcosm of the trends, tensions, and opportunities of Brazil's new green economy.

The main conclusion is that the network is not a monolithic block, but rather a functional architecture divided into two highly specialized poles: the field "solution providers" and the strategic "demanders" and "facilitators".

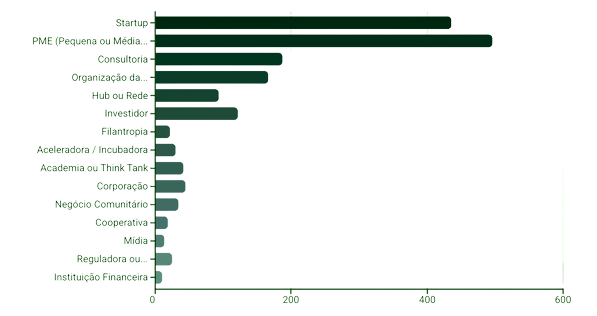

The horizontal bar chart illustrates the distribution of organization types, highlighting the predominance of Small and Medium Enterprises (SMEs) with 496 entities, and Startups with 436. Consulting firms also represent a significant share with 187, underlining the demand for specialized expertise. Civil Society Organizations (CSOs/NGOs) and Investors (including Venture Capital and Impact Funds) are crucial players, with 166 and 122 organizations respectively, reflecting the hybrid nature and growing financial interest in the sector. Entities such as Academia, Corporations, and Incubators, although fewer in number, play strategic roles in innovation and scalability.

Method

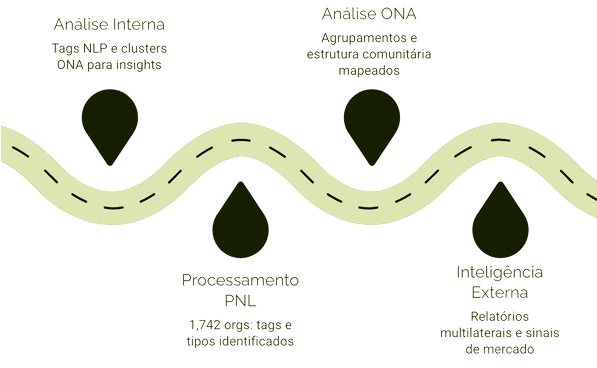

The map is constructed from a rigorous quantitative analysis of approximately 1800 organizations using Natural Language Processing (NLP) and Organizational Network Analysis (ONA), combining external market intelligence and creating a 360° view of the bioeconomy ecosystem. The methodology allows us to map not only “what exists” (organizational structure), but also “why it matters” (market context) and “where it’s going” (trends and opportunities). This convergence of internal data and external signals reveals patterns invisible in isolated analyses, such as the discovery of two parallel universes and the identification of the strategic bridges needed to connect them.

"Tags" and the galaxy of Nature-based Solutions (NbS)

Delving deeper into the ecosystem's internal structure, our analysis revealed the predominant themes and areas of activity, categorized by "tags." This mapping allows us to visualize the driving forces and focuses of innovation and impact within Nature-based solutions in Brazil. The tags reflect the main narratives and specializations of the actors that make up the NbS galaxy.

The image shows a complex network visualization with interconnected nodes representing the 1,742 organizations in the ecosystem of Nature-based solutions.

The nodes appear in different sizes and colors, connected by lines that show the relationships between the organizations. In the center there is a denser cluster with "SMEs, Small and Medium Enterprises" highlighted, surrounded by other types of organizations such as startups, consultancies, NGOs, investors, etc.

The visualization reveals the network structure of the ecosystem, showing how different types of organizations group together and connect, forming a "galaxy" of actors in nature-based solutions in Brazil.

The two parallel universes

Solution providers

On one side are the "suppliers" in the field, the "ground" of the biodiversity economy. This pole is led by SMEs (Small and Medium Enterprises), which have an approximately 78% implementation profile and are the main drivers of the Bioeconomy and Ecological Restoration. Alongside them are CSOs (Civil Society Organizations), with an approximately 70% implementation profile, focusing on community development and Biodiversity/Conservation. Cluster analysis confirms that this is the heart of the bioeconomy, a dense group focused on the territory.

Strategic demanders and facilitators

On the other side, there is the strategic cluster, the "agenda world," which constitutes a coalition of specialized clusters. This pole is formed by Consulting firms (approximately 72.5% driving forces), which respond to the growing corporate demand for ESG; by Investors (± 66%), who provide Capital; and by Academia (± 69%), which provides Research & Development.

The bottlenecks of the SbN ecosystem

The financial bottleneck

The funding analysis exposes the financial "desert" of this ecosystem. There is a profound gap between venture capital and philanthropic capital. On one hand, investors and accelerators prioritize scalable technology theses. Investors focus on Impact Finance/VC and Climate Tech, both central themes for the ecosystem's "facilitators" and "demanders." Notably, these actors demonstrate very little interest in "ground-level" solutions, such as Bioeconomy (only 1.8% of investor focus) or Community Development (1.3%). On the other hand, philanthropy assumes the role of financing the public good, concentrating massively on Biodiversity/Conservation (18.5%) and Community Development (7.6%).

The critical gap lies with SMEs (the “Providers”). As we have seen, they are the main drivers of the Bioeconomy (22.7% of their focus) and Ecological Restoration (10.9%). These “field” businesses are neither tech-savvy enough for venture capital nor purely charitable enough for traditional philanthropy. This “gap” is a documented challenge in the sector.

The opportunity is clear: to use Blended Finance — a thesis in which Philanthropy itself has already shown interest (5.4%) — to act as catalytic capital. This action, perfectly aligned with the Federal Government's Ecological Transition Plan and the new BNDES fund strategies, aims to "de-risk" these bioeconomy projects in order to finally attract a large volume of private investors.

Deepening Capital Flows: The Abyss

The disconnect between the engine of technological innovation and the vast potential for socio-environmental impact is the central challenge of our bioeconomy and nature-based solutions ecosystem. Our data clearly show that this gap is perpetuated by the way capital flows, or rather, how it *doesn't* flow between these two worlds. There are two financing systems operating in parallel, rarely intersecting, and it is this separation that creates the "chasm".

FLOW A: VENTURE CAPITAL

Dominated by 122 VCs and 30 Accelerators, this capital seeks scale and recurring revenue models, such as SaaS. The language is Impact Finance and Climate Finance, directing investments towards Universe A (Startups) that operate with Carbon Credits and Regenerative Agriculture.

FLOW B: PATIENT CAPITAL

Comprising 22 Foundations (Philanthropy), this stream focuses on Community and Territorial Development. It represents patient capital that respects the longer cycles of the forest and social impact, directly supporting the B Universe (SMEs and Traditional Communities).

The geographical bottleneck

Of the 1,742 organizations analyzed, the Atlantic Forest concentrates the largest number (320 organizations), followed by the Amazon (280 organizations) and Cerrado (180 organizations). However, despite these numbers, the Amazon stands out as a global brand of natural capital and a historical focus of philanthropic investments, creating a paradox between the physical presence of the organizations and market attention.

The ecosystem is, today, fundamentally "Amazon-centric." The overwhelming majority of actors, from SMEs to academia, concentrate their focus of activity in the Amazon. While this validates the biome as the great engine of the national bioeconomy, this massive concentration creates "deserts" of innovation and investment in other biomes that are equally critical to national security.

The biggest gap is the extremely low representation of the Atlantic Forest – the most populous biome, which governs the water and energy security of more than 70% of Brazil's GDP – and the Cerrado, the agricultural frontier with immense deforestation pressure and the main source of emissions from land use.

Meanwhile, Corporations (40%) and Startups (18.7%) dominate the Sustainable Cities niche, a crucial gateway to the Atlantic Forest, but one that still needs solutions that go beyond waste management and embrace urban green infrastructure and forest restoration for water protection.

Bridges: Connections and Strategic Solutions

The gap in connection between strategic “demanders” and “facilitators” and field “suppliers” is the central challenge. The opportunity lies with the most hybrid actor in the ecosystem: startups. With a profile almost perfectly divided between these two universes (approximately 51% vs. 48%), they are the natural bridge. They create both digital platforms (facilitators) and circular economy solutions (suppliers). The key to the ecosystem's maturity is, therefore, to use this hybrid profile to build three strategic bridges:

An important cross-cutting element: Market development must be accompanied by technical assistance and training for implementers.

Bridge 1: Financial

Mechanisms: Utilize Blended Finance and Venture Philanthropy.

Venture Philanthropy reduces the risk of investing in early-stage organizations, making them more attractive to traditional capital.

Actions and Actors: Use startups with these mechanisms to mobilize capital. Venture Philanthropy is crucial to helping businesses in need of philanthropy enter the market, benefiting both startups and community-based businesses. Startups and Blended Finance mechanisms connect the capital pole (“demanders”) to the execution pole (SMEs, “providers”), proving the viability and scalability of bioeconomy and restoration businesses.

Bridge 2: Market

Mechanism: Connect the strong corporate demand for ESG (currently met by consulting firms) directly to projects with real impact at the grassroots level (SMEs and NGOs).

This transforms corporate sustainability goals into direct investment and funding for conservation and

community development.

Actions and Actors: Startups: Meet the corporate demand for scalable solutions. Community-Based Businesses : Become sources of Sustainable Sourcing (sustainable inputs, carbon credits) for large companies.

Bridge 3: Technological

Applying digital innovation (Digital Platform/SaaS, AI, Geotechnology) to

Startups to scale, monitor, and bring traceability to SME projects and

CSOs. This bridge is not just an optimization; it is a market survival necessity to guarantee access to international markets, which now demand greater transparency, socio-environmental compliance, and proof of robust monitoring throughout the value chains.

Actions for Startups: Apply digital platforms (SaaS, AI) to reduce monitoring , traceability , and technical assistance costs (MRV – Measurement, Reporting, and Verification). Actions for Community-Based Businesses: Provide internet access, online training, and access to digital marketplaces, overcoming territorial isolation.

In short, the network reveals a mature and specialized ecosystem. Its next stage of evolution will not come from the creation of more actors, but rather from the deliberate strengthening of strategic connections between the worlds that compose it.

Team

Daniel Contrucci

Laura Fostinone

Luiz Bouabci and Mariana de Salles

Victor Solomon

Syntropics

Our Partners

We work in collaboration with organizations and institutions committed to the climate agenda and sustainable development, including:

These partners play a crucial role in the development and implementation of the solutions and analytics presented by OV Insights.

![]()